Overview

Boston, MA

November 2003

The Battle for the US Consumer: FDC, Wal-Mart, and the Future of the Payments Industry

NEW RESEARCH REPORT BY MERCATOR ADVISORY GROUP

The Wal-Mart settlement helps the large merchants save money because they can now more easily negotiate rates with acquirers and banks. Meanwhile, small and medium size merchants end up paying a predominant share of the settlement costs because they have little to negotiate with -- but of course ultimately it is the consumer that will pay the $3 billion settlement.

"The Battle for the US Consumer: FDC, Wal-Mart and the Future of the Payments Industry" argues that the Wal-Mart settlement is the opening salvo of a war, not the end of a skirmish. This new war is driven by banks and merchants that have a shark-like affinity for consumers, and the Wal-Mart litigation is simply the first sign that merchant consolidation/cooperation has introduced a new power that the payments industry must reckon with.

In the past, merchants were almost exclusively concerned about cost control. Today merchants are focused on driving consumer loyalty so that the merchant gets an increased share of the consumer's wallet. To achieve consumer loyalty merchants need the same type of consumer knowledge that was once the exclusive domain of the banks. Tim Sloane, author of the report, states that "merchants are keenly aware of the benefits that come from owning the point-of-sale (POS) and the direct customer relationship; goals almost identical to the banks. As a result I expect these conflicts will increase and merchants will experiment with new technologies that can further solidify their loyalty programs and their control over consumer payment options."

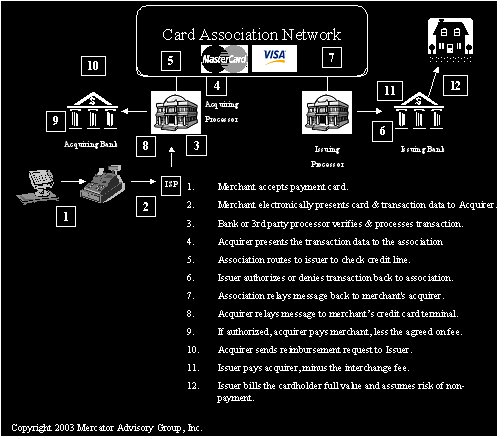

The Wal-Mart litigation has dramatically altered the long-term battle for the U.S. consumer spending by re-establishing the role of a free-market economy for PIN-based online payment. This court finding is in essence a new court defined boundary that identifies the online PIN-based products as distinct offerings from the larger general-purpose card market. By declaring Online Debit as a unique product from Offline, the court has effectively taken Online Debit out of the control of the existing bank associations.

While this court decision appears to be black & white, the current market implementation of PIN-based online payment is not. Existing contractual obligations, pricing, and agency/duality issues abound; and untangling the products will present a huge new business opportunity and likely legal battlefield.

This report contains 28 pages and 6 exhibits.

Members of Mercator Advisory Group have access to these reports as well as the upcoming research for the year ahead, presentations, analyst access and other membership benefits. Please visit us online at www.mercatoradvisorygroup.com.

For more information call Mercator Advisory Group's main line: 508-845-5400 or send email to [email protected].

Make informed decisions in a digital financial world