Overview

Trillions of dollars and billions of transactions pass through the branded network payment systems of Mastercard and Visa. A small fraction of these transactions end up as payment disputes. These flawed transactions are indications of unauthorized use, family fraud, unsatisfactory merchandise, or errant claims. Best estimates are that 4 basis points, or 4/1000ths of transaction volumes fall into this category. As we hit the next decade, expect exceptions to number nearly 25 million units.

Codified rules and network regulations protect consumers, but at a handling cost of $20–25 per unit, the cost to credit card issuers to investigate and resolve disputes exceeds $500 million. Payment networks are in the process of revamping their dispute processes, going beyond current regulations to collape resolution parameters, create efficiencies, and level the issuer-merchant playing field.

Mercator Advisory Group’s new research report explains payment network process enhancements that go beyond the requirements of regulatory standards. It discusses what payment technology firms are doing to improve satisfaction for customers, issuers, and merchants. Readers will learn how to leverage the investment made in reconciling these accounts into a strategic advantage that can help mitigate fraud and ease the cardholder’s burden.

“Every credit card issuer requires its transactions to be irrefutable, but there will inevitably be flawed items along the way,” comments Brian Riley, Director, Credit Advisory Service at Mercator Advisory Group, the author of the research report. “Not every customer’s complaint is right, but many times disputes can help identify fraud risk. Payment technology firms make it easier to reconcile these errant transactions. Credit card issuers must think of their dispute units as an asset, not a burden. Don’t forget, there is plenty of data in these transactions that can be used to assess risk and mitigate loss.”

This research report is 21 pages long and has 9 exhibits.

Companies mentioned in this research report include: American Express, Baldwin Hackett & Meeks, Bank of America, Barclays, Capital One, Chase, Citi, Discover, Ethoca, FICO, Fiserv, Mastercard, Pegasystems, TSYS, and Visa.

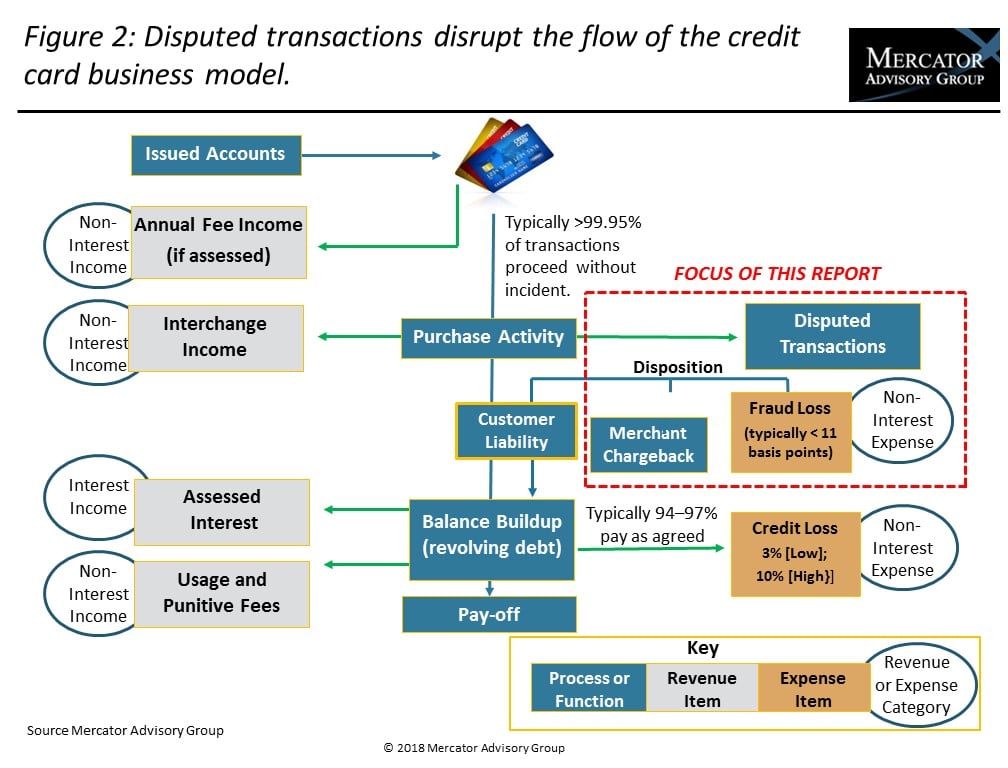

One of the exhibits included in this report:

- Payment development to improve the process

- Dispute management as a strategic tool

- Forecasted transaction number and dollars through 2022

- Fraud losses by type

- How top technology companies add value

Make informed decisions in a digital financial world