Overview

Readers will get a deeper understanding of credit risk in this year’s report along with a detailed explanation of how the credit card delinquency process works. Early and late delinquencies have a direct impact on credit card profitability, which is expressed through the return on assets (ROA) metric. In the United States, credit card ROA has been steadily falling from the 4.94% achieved in 2014. In this report, Mercator projects 2.4% ROA for 2020.

“As 2019 begins, card issuers need to be planning for 2020 and should expect slower growth, slimmer profits, and tighter lending,” commented Brian Riley, Director, Credit Advisory Service, at Mercator Advisory Group, the author of the research report. “Pay attention to how top issuers are keeping their portfolios in check, as issuers outside of the top 100 are seeing severe risk. In 2018, top issuers experienced credit losses of 3.81% of their receivables while those outside of the top 100 saw their rates surge to 7.92%. If this persists, some market consolidation is likely,” Riley continued.

This research report contains 24 pages and 16 exhibits.

Companies mentioned in this research report include: Bank of America, Chase, Citi, and FICO.

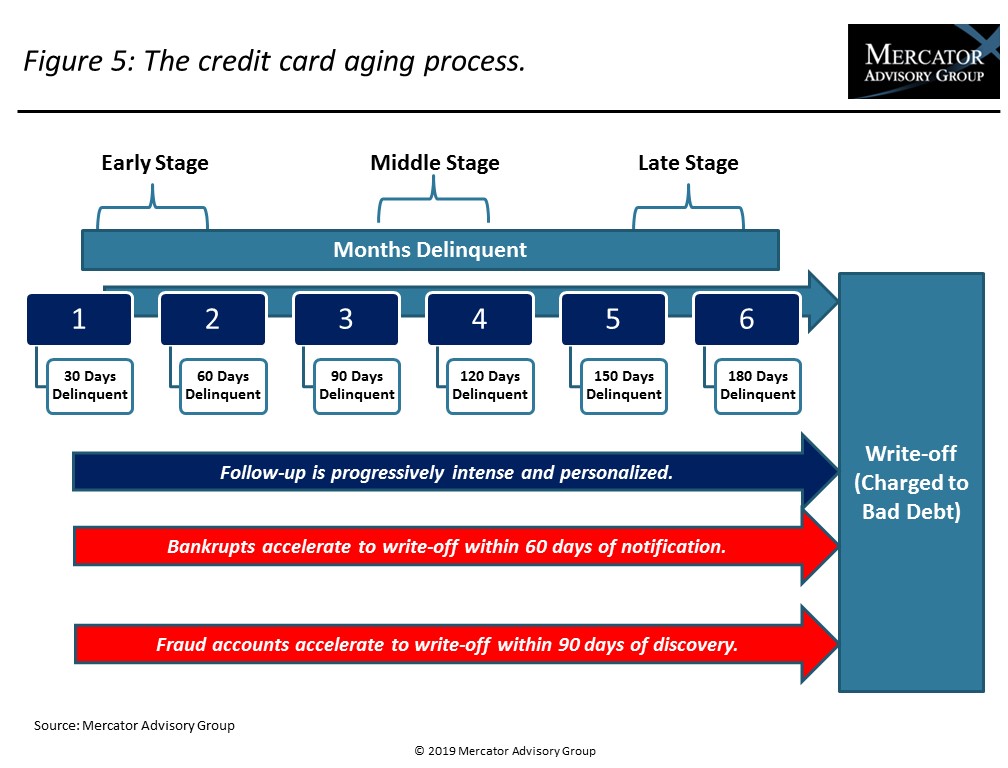

One of the exhibits included in this report:

- Revolving debt forecasted through 2022

- Projected U.S. household debt through 2021

- Anticipated U.S. credit card account growth through 2022

- New, early, and late delinquency volumes through 2020

- Prime lending rates, new accounts, and disposable household budgets through 2020

Make informed decisions in a digital financial world