Overview

Mercator Advisory Group’s most recent Insight Summary Report, Omnichannel and Branch Banking: Making It Personal, from the Banking and Channels Survey in the bi-annual CustomerMonitor Survey Series, a part of Mercator’s Primary Data Service, reveals that consumers want their financial institution to know them better.

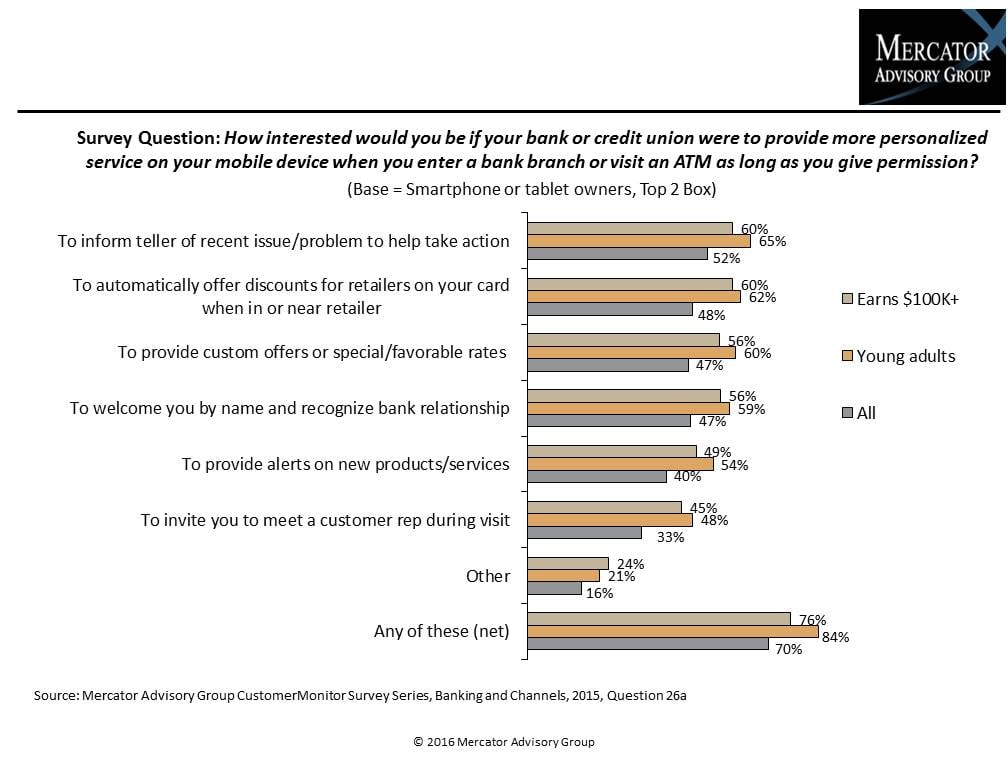

Our survey suggests that 3 in 4 U.S. adults own smartphones or tablets, and 70% of them would be interested in their financial institution providing more personalized service to them on their mobile device when they enter a branch of their bank or credit union or use an ATM if they grant permission. Bluetooth low energy (BLE) technology is one way that financial institutions can provide personalized service by using beacons to transmit custom messages to customers’ mobile devices based on the individual’s location. Mobile accessibility supports deeper customer relationships and offers greater convenience.

Consumers are most interested in using this technology to inform tellers or branch personnel of a recent issue or problem when they enter the branch so they can take action, mentioned by over half of consumers with mobile devices. They are next most interested in automatically being offered discounts at retailers when they are in or near a store for purchases using their bank-issued payment cards. Each usage is of interest to roughly half of mobile consumers and 60% of high-income earners and even more young adults. Half of mobile consumers would simply like to be welcomed by name with recognition of their banking relationship, rather than having to swipe their debit or bank card when they reach the teller, or would like to be alerted of special, custom offers or favorable rates.

In fact, 13% of all consumers surveyed indicated they frequently encountered their FI did not recognize a problem or issue that they previously reported. Young adults (27%) and high income earners whose household earns $100,000 or more a year (23%) are even more likely to notice this. While few customers switched banks due to previous customer service issue with their FI, more switched because their new FI knows them better.

Consumers are demanding a new kind of retail bank that blends a physical presence with digital technology for quicker service and access to a deeper knowledge base. Banking customers and credit union members increasingly expect their financial institution (FI) to recognize them and know their individual situation based on their portfolio there and their communications with the FI via multiple channels used. Meeting those expectations will yield a truly omnichannel retail banking institution of the future that offers a more personalized approach to banking.

Banks and credit unions are redesigning the branch experience to draw in new customers and engage existing customers in a variety of ways. The branch is becoming an advice center with more personalized services, and not just for transactions. With the growth of online and mobile banking and broader deployment of ATMs and other self-service channels, more transactions can be done outside the branch. Yet, branches remain the center of most retail customers’ banking world, where they can speak with and interact with knowledgeable personnel on important issues that cannot be solved as easily through self-service methods.

The report, Omnichannel and Branch Banking: Making It Personal shows that branches are still an important center for consumer banking but the traditional branches are changing to accommodate consumers’ new demands. It presents the findings from Mercator Advisory Group’s CustomerMonitor Survey Series online panel of 3,008 U.S. adult consumers surveyed in November 2015.

This study examines the demographic shifts, types of relationships with financial institutions, use of bank branches compared to other banking channels, and frequency of branch visits and identifies trends in consumers’ methods of communicating with their bank and frequency of contact, perceptions of an ideal branch, interest in in-branch videoconferencing, and mobile-based personalization. It identifies opportunities for cross-selling and opportunities for improving the banking customers’ omnichannel experience.

“The branch remains a vital component of the banking relationship, but consumer expectations are changing. Young adults, high-income earners, and mobile banking users are more likely than average to visit the branch, but not necessarily for simple transactions,” states Karen Augustine, manager of Primary Data Services including CustomerMonitor Survey Series at Mercator Advisory Group and author of the report.

The report is 76 pages long and contains 31 exhibits.

One of the exhibits included in this report:

Highlights of this report include:

- Year-over-year trending of the number/types of financial institutions used by consumers, the institutions they consider their primary FI, usage of the primary institution’s credit card, and types of financial advisors

- Shifts in communication methods with FIs and satisfaction with those methods

- Consumers’ preferred type of branches

- New account openings by type of account by method, and experience with account opening

- Reasons for branch usage, frequency of visits, and interaction with branch staff

- Interest in becoming aware of relevant new financial products and services and preferred methods of learning about them

- Interest in mobile-based personalization when visiting a bank branch or ATM

- Trends in use of and interest in in-branch videoconferencing with product specialists or teller-assisted videoconferencing for conducting transactions

- Frequency of cross-platform issues, delays or redundancies in information needed

Make informed decisions in a digital financial world