Overview

Mercator Advisory Group’s most recent Insight Summary Report, based on the annual Payments survey in the CustomerMonitor Survey Series, conducted in June 2016, reveals that retailer cards is among the fastest growing categories of prepaid cards tracked this year.

Consumers and Prepaid: Growing Use, Especially for Retailer-Specific Cards, the latest report from Mercator Advisory Group, presents survey findings based on responses to an online survey of 3,009 U.S. adults conducted in June 2016 as part of the CustomerMonitor Survey Series. The report examines a demographic shift of prepaid card and virtual card buyers and the changing landscape of prepaid card use and recalled loads, highlighting eight categories of prepaid card types. Survey findings cover usage, frequency, distribution channels, the relative importance of feature sets and fees, and brand awareness and current or previous use of 11 major brands of general purpose reloadable cards, reasons for discontinuing use, as well as awareness and use of direct deposit onto general purpose reloadable (GPR) cards.

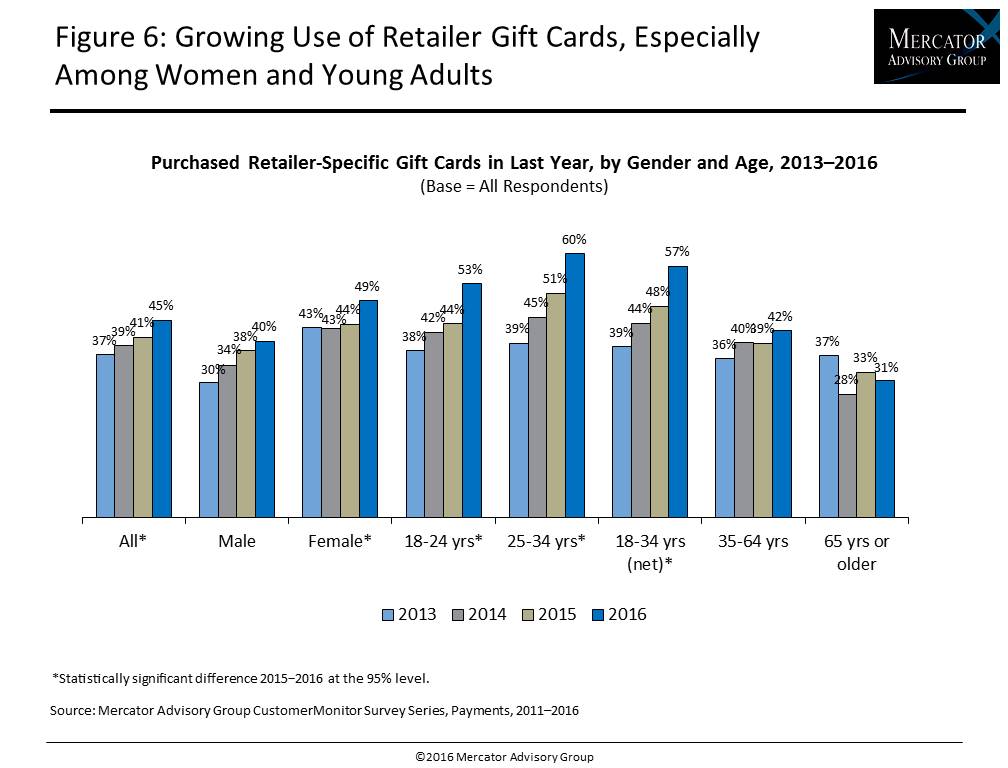

The survey finds that 63% of U.S. adults bought prepaid cards in year preceding the June 2016 survey, up from 61% in 2015 and 56% in 2014. Retailer-specific cards are the most popular type of prepaid cards, bought by 45% of U.S. adults, up from 41% in 2015. Much of the growth in prepaid, and now, even in retailer-specific cards is from young adults, particularly 25–34 year olds. Retailer specific cards are typically bought by consumers of all ages, but recently, young adults are most likely to buy even retailer-specific cards, nearly 3 in 5 young adult respondents indicating they bought them during the previous year, up from less than a half of young adults who did so in the 2015 survey. As retailers introduce new mobile apps, often with mobile payment options that include their retailer prepaid cards, young adults begin to buy retailer cards for their own use, so the cards are becoming a primary payment tool and not just used as gifts.

Women continue to be more likely than men to buy retailer-specific cards, as 49% of women but only 40% of men bought this type of card within the previous year. However, the number of men buying retailer-specific cards has grown steadily since Mercator Advisory Group began tracking purchase of this type of prepaid card in 2013.

“Retailers are introducing more mobile-based apps and offers when using their loyalty and prepaid programs, which may be fueling this growth in retailer gift card purchases. Young adults continue to lead this mobile revolution and growing use of prepaid cards as a money management tool,” states the author of the report, Karen Augustine, manager of Primary Data at Mercator Advisory Group including the CustomerMonitor Survey Series.

The report is 71 pages long and contains 32 exhibits.

Companies mentioned in this report are: American Express, Chase, Green Dot, H&R Block, NetSpend, PayPower, Rush, and Walmart.

One of the exhibits included in this report:

Highlights of this survey and report include:

- Year-over-year trending of prepaid card use by eight categories of prepaid cards (including retailer-specific, general purpose, and reloadable cards) and consumers’ recollection of cards purchased and monthly load volume

- Shifts in the demographics of prepaid card and virtual card users and the ways consumers use them

- Locations used to buy prepaid cards and virtual cards, for self and as gifts

- Awareness and use of online gift card exchanges

- Purchase behavior regarding GPR cards, including length of time card is in use, load frequency, and awareness and use of direct deposit to GPR cards

- Brand awareness, purchase, timing, and current use of 11 GPR card brands

Make informed decisions in a digital financial world