Overview

P-to-P Payments at Financial Institutions: Not Micro, Not Mobile, Not Personal

Boston, MA -- Financial institutions offering P-to-P services have discovered that consumers will find innovative uses for new products that the designers often never envisioned. While many financial institutions began offering person-to-person (P-to-P) products with the expectation that they would be used to make small dollar payments between individuals, consumers have latched onto these products as a way to make a wide range of electronic payments and eliminate checks.

Banks and credit unions thought that P-to-P products would be used for payments around $20, but many have found the average size of the payments are ten times that amount! This means that the P-to-P market is much more than consumers splitting a restaurant tab. This market includes other payments such as those between an individual and a small business that does not have an electronic invoicing or payments system. Even so, paying the babysitter or the dog walker is not the same payment function as taking care of a utility or credit card bill, nor is it purely personal.

Revealed in Mercator Advisory Group's P-to-P Payments at Financial Institutions: Not Micro, Not Mobile, Not Personal report is how banks and credit unions may benefit from the application of these products both by leveraging them as a way to encourage electronic means for payments that were once the domain of cash and checks and by charging a reasonable fee for a service that provides value to their customers.

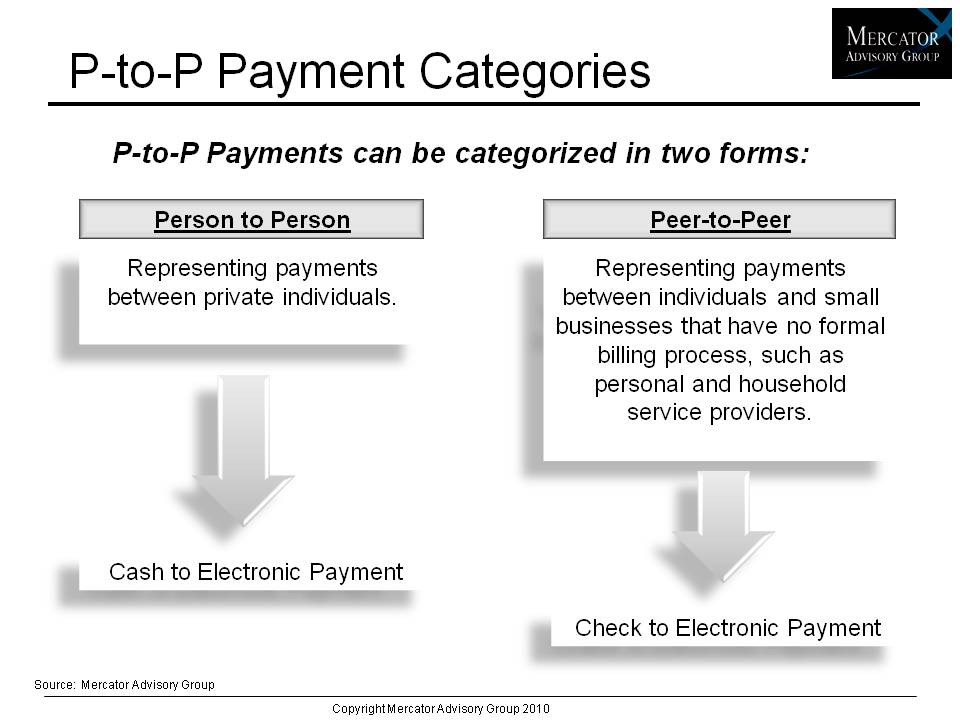

"It may be more accurate to refer to these kinds of payments as 'peer-to-peer' payments, as some industry analysts already do. This is because both the sender and the recipient are peers in that their use of electronic billing and payment systems happens through a common set of financial transaction tools," Ben Jackson, senior analyst in Mercator's Prepaid Advisory Practice comments.

The report focuses on the emerging U.S. market for P-to-P payments delivered through financial institutions.Mercator Advisory Group explores current offerings from major banks and credit unions, outlines who some of the major vendors are, examines the types of payments being made using these services, and reviews the market opportunity. This report begins to define how the P-to-P market is starting to segment itself as solutions, delivery channels, and users enter their second stage growth phase.

Highlights of the report include:

Financial institutions are rapidly enabling 'P-to-P' payments functions as part of their online bill payment systems, but real-time transfer capabilities are now entering the market.

The average transaction size made with 'P-to-P' services is larger than expected, showing a market for person-to-business transactions out of P-to-P products.

Financial institutions seem unclear on whether P-to-P payments are a revenue generator or a customer retention tool. The question remains unanswered, and it might be up to vendors to help institutions get comfortable with certain fee strategies.

Consumers seem ready to adopt the service, and vendors' surveys show that customers feel secure about conducting these transactions through their financial institutions.

Our analysis suggests that this service could provide a significant new revenue source even with only small charges per transaction.

One of the 10 figures from the report:

This report contains 29 pages and 10 exhibits.

Members of Mercator Advisory Group have access to this report as well as the upcoming research for the year ahead, presentations, analyst access and other membership benefits.

Please visit us online at www.mercatoradvisorygroup.com.

For more information and media inquiries, please call Mercator Advisory Group's main line: (781) 419-1700, send E-mail to [email protected].

Follow us on Twitter @ http://twitter.com/MercatorAdvisor.

About Mercator Advisory Group

Mercator Advisory Group is the leading, independent research and advisory services firm exclusively focused on the payments and banking industries. We deliver pragmatic and timely research and advice designed to help our clients uncover the most lucrative opportunities to maximize revenue growth and contain costs. Our clients range from the world's largest payment issuers, acquirers, processors, merchants and associations to leading technology providers and investors.

Make informed decisions in a digital financial world